99% 4. 159% Source: U.S. Dept. of Housing and Urban Development, 2015 With their unique requirements and terminology, FHA home loans can be a little confusing and challenging. These loans are a bit different from standard mortgages because they are government-backed. Understanding these distinctions can help you avoid mortgage incidents and improve deals for your funding.

Click the links to explore subjects more thorough. Homeownership has actually long been considered the foundation of the American Dream. The majority of U.S. people are homeowners, and for many, residential or commercial property is their primary source of wealth. Yet, before the FHA was created in 1934, the United States was a country of tenants.

These requirements made it tough for the majority of people to own homes. The FHA was created to help the U.S. emerge from the Great Anxiety and to assist Americans purchase houses. In 1965, it ended up being part of the U.S. Department of Real Estate and Urban Advancement (HUD). Over the years, the realty and home mortgage markets have actually altered substantially, and FHA programs have actually continued to progress to support American homebuyers and homeowners.

Typical 2018loan amount Portion of FHA purchase loans to novice buyers in 2018 83% 8 million Sources: FHA Single-Family Origination Trends Report, August 2018; FHA Annual Mgmnt Report, 2018 FHA underwriting standards, eligibility requirements and insurance premiums alter all the time the firm must stabilize the requirements of homebuyers with a mandate to safeguard taxpayers from losses.

Fascination About Which Banks Are Best For Poor Credit Mortgages

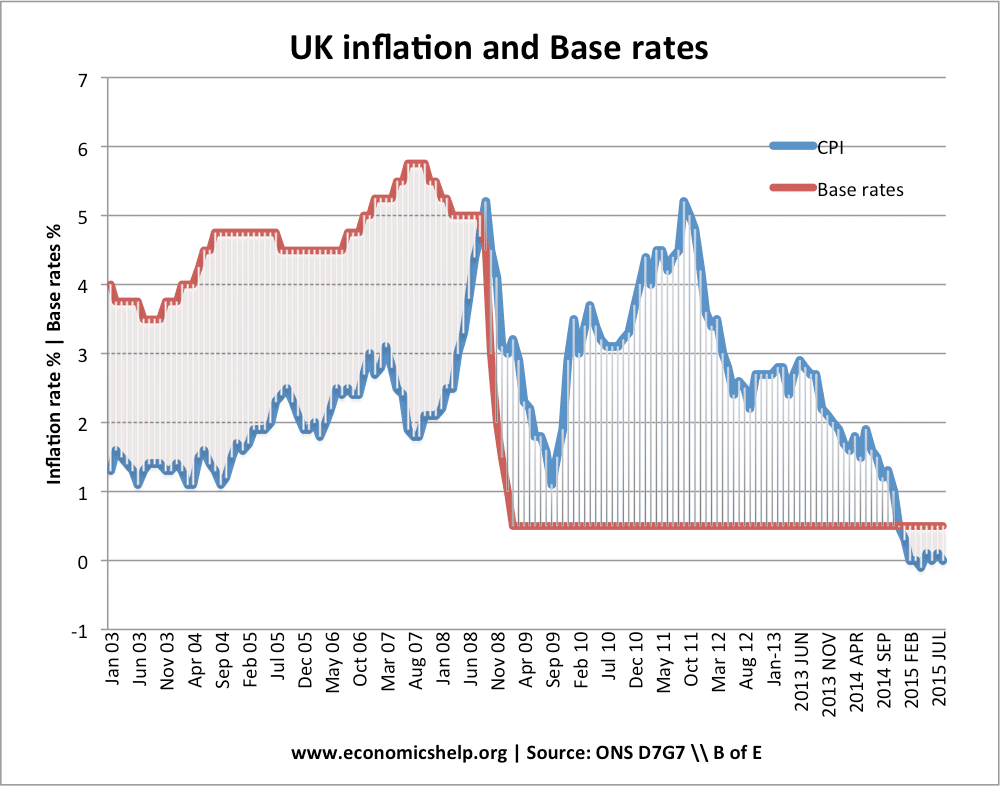

For instance, in early 2008, prior to the financial crisis, nearly half of the authorized FHA loans went to debtors who had a FICO rating listed below 620, according to the FHA's 2014 annual report to Congress. The Great Economic downturn and home loan foreclosure crisis have pushed that percentage down to less than 5 percent of authorized customers, as you can see in among the charts listed below.

FHA's Market Share Because Year 2000 Source: Federal Real Estate Administration 2015 FHA Borrowers Credit Rating Distribution Source: Federal Real Estate Administration 2015 You need to comprehend that average credit history are just that averages. FHA lending institutions take a look at the whole application plan payment history, income stability, properties, deposit and more. Lower ratings are not constantly the result of bad credit, and lending institutions acknowledge that. what are the main types of mortgages.

Candidates with greater debt-to-income ratios, smaller sized deposits or other weaknesses typically require scores that surpass the bare minimums. The FHA program is not the only choice for individuals with small deposits who wish to purchase homes. Here are other options you can check out. Both Fannie Mae and Freddie Mac offer 97 percent mortgages to eligible newbie homebuyers.

Nevertheless, they have a couple of advantages over FHA loans: The down payment is simply 3 percent. There is no upfront mortgage insurance coverage, and the annual premiums are lower. Borrowers can ask for mortgage insurance coverage cancellation when the loan balance drops to 80 percent of the initial house value. If you have actually owned a house in the last three years, you don't receive this loan however you may still have the ability to get a standard loan with a 5 percent deposit.

The 25-Second Trick For How Much Are The Mortgages Of The Sister.wives

Some house sellers are willing to finance their own homes. The purchaser may have the ability to avoid lender costs and other homebuying expenses like title insurance coverage. Sellers might be more ready than home loan lenders to overlook credit or income issues. Nevertheless, purchasers of owner-financed homes need to have an appraisal done to avoid overpaying for the residential or commercial property.

Specific sellers don't have to play by the exact same guidelines as licensed home mortgage loan providers, which suggests that customers have fewer defenses. FHA is not the only federal government home loan program. VA and U.S. Dept. of Agriculture (USDA) home mortgage offer a number of advantages over FHA loans for those who are qualified.

Department of Veterans Affairs guarantees home mortgages for qualified service members, veterans, and in some cases relative. These loans do not have deposit requirements, and debtors don't need to pay month-to-month home mortgage insurance. Frequently supplied in rural locations, USDA loans permit qualified debtors to get a mortgage without a down payment when they buy a home in a qualified area (how to rate shop for mortgages).

residents reside in areas qualified for USDA loans. USDA home mortgages have funding charges (2 percent), which can be funded, https://ygeruseikv.doodlekit.com/blog/entry/16663966/getting-my-how-do-collateralized-debt-obligations-work-mortgages-to-work and require annual home mortgage insurance, but the premiums are lower than FHA insurance. The FHA mortgage was developed to meet the requirements of homebuyers who have smaller sized deposits it doesn't matter the number of houses they have actually owned.

9 Simple Techniques For When Will Student Debt Pass Mortgages

A purchaser with a smaller down payment may still be much better off with a standard loan it truly depends on the total package. when does bay county property appraiser mortgages. Property buyers ought to compare the total expenses of traditional and FHA provides from contending loan providers to make sure they are selecting the lowest-cost choice that best meets their special requirements.

Both FHA and conventional mortgage rates are set by personal lenders, not the government. Costs and rates differ amongst home mortgage lending institutions by approximately 0. 25 to 0. 50 percent. Rates and terms can alter regularly. Home loan insurance coverage expenses also alter in time. Property buyers with less than 20 percent down must compare both conventional and FHA loans when they purchase home loans.

There is no mandatory guideline due to the fact that FHA mortgage are made by private mortgage lending institutions, and they set their own rates and charges. FHA loan providers might also impose higher standards than the FHA needs these standards are called overlays. FHA mortgage underwriting is a few of the most forgiving in business.

5 percent loan), proven earnings that is continuous, adequate and steady, funds to cover the down payment and closing expenses, and a debt-to-income ratio that does not exceed 43 percent. Those are the basics. Candidates who surpass these Click for more info minimum qualifications have a better opportunity at loan approval, and those who barely satisfy standards may need to work harder to get a loan.

See This Report about Which Congress Was Responsible For Deregulating Bank Mortgages

Most house loans (consisting of FHA) are underwritten with automated underwriting systems (AUS), which provide decisions in seconds. Those with less common scenarios consisting of no reported credit rating, all-cash down payments or identity theft need to be underwritten by hand, which can take longer. On average, home loans close in about 40 days.

Only if the seller's representative has an incorrect view of FHA loans. Some believe that FHA needs higher property requirements and needs sellers to pay buyer's expenses not real. Others do not like the FHA Amendatory Clause, which permits purchasers to cancel a purchase if the home does not appraise for a minimum of the prices.

Some perceive FHA borrowers as borderline and more difficult Website link to approve an impression that can be overcome by getting loan approval before purchasing a home. One downside of FHA house loans is that customers can not drop FHA home mortgage insurance coverage, even when the loan-to-value ratio drops listed below 80 percent. If a homebuyer keeps an FHA loan for an entire 30-year term, it might be pricey.