This implies you'll require to make a down payment of 3. 5%. You'll need a credit history of at least 580 to certify. If your credit score falls in between 500 and 579, you can still get an FHA loan as long as you can make a 10% down payment. With FHA loans, your down payment can originate from cost savings, a monetary gift from a relative, or a grant for down-payment support.

Federal Real Estate Administration (FHA) loans are federally-backed home loans developed for low-to-moderate-income borrowers who may have lower than typical credit report. Federal Real Estate Administration (FHA) loans require a lower minimum down payment and a lower credit rating than lots of standard loans. Federal Real Estate Administration (FHA) loans are issued by FHA-approved banks and financing institutions; these institutions will evaluate your certifications for the loan.

It is essential to keep in mind that with an FHA loan, the FHA doesn't in fact lend you cash More helpful hints for a home loan. Instead, you get a loan from an FHA-approved lending institution, like a bank or another financial organization. However, the FHA ensures the loan. after my second mortgages 6 month grace period then what. Some individuals refer to it as an FHA insured loan, because of that.

Your loan provider bears less threat since the FHA will pay a claim to the lending institution if you default on the loan. While Federal Federal Housing Administration Loans (FHA Loans) need lower deposits and credit report than conventional loans, they do carry other stringent requirements. For How Long You Pay the Yearly Mortgage Insurance Coverage Premium (MIP) 15 years 78% 11 years 15 years 78.

What Does Why Is There A Tax On Mortgages In Florida? Mean?

01% to 90% 11 years > 15 years > 90% Loan term Congress created the Federal Real estate Administration in 1934 throughout the Great Anxiety. At that time, the real estate industry was in problem: Default and timeshare nation foreclosure rates had escalated, loans were restricted to 50% of a residential or commercial property's market value and mortgage termsincluding short repayment schedules coupled with balloon paymentswere difficult for many property buyers to satisfy.

was mostly a country of occupants, and only roughly 40% of homes owned their homes. In order to stimulate the real estate market, the government developed the FHA. Federally-insured loan programs that lowered lender risk made it simpler for borrowers to receive home mortgage. The homeownership rate in the U.S.

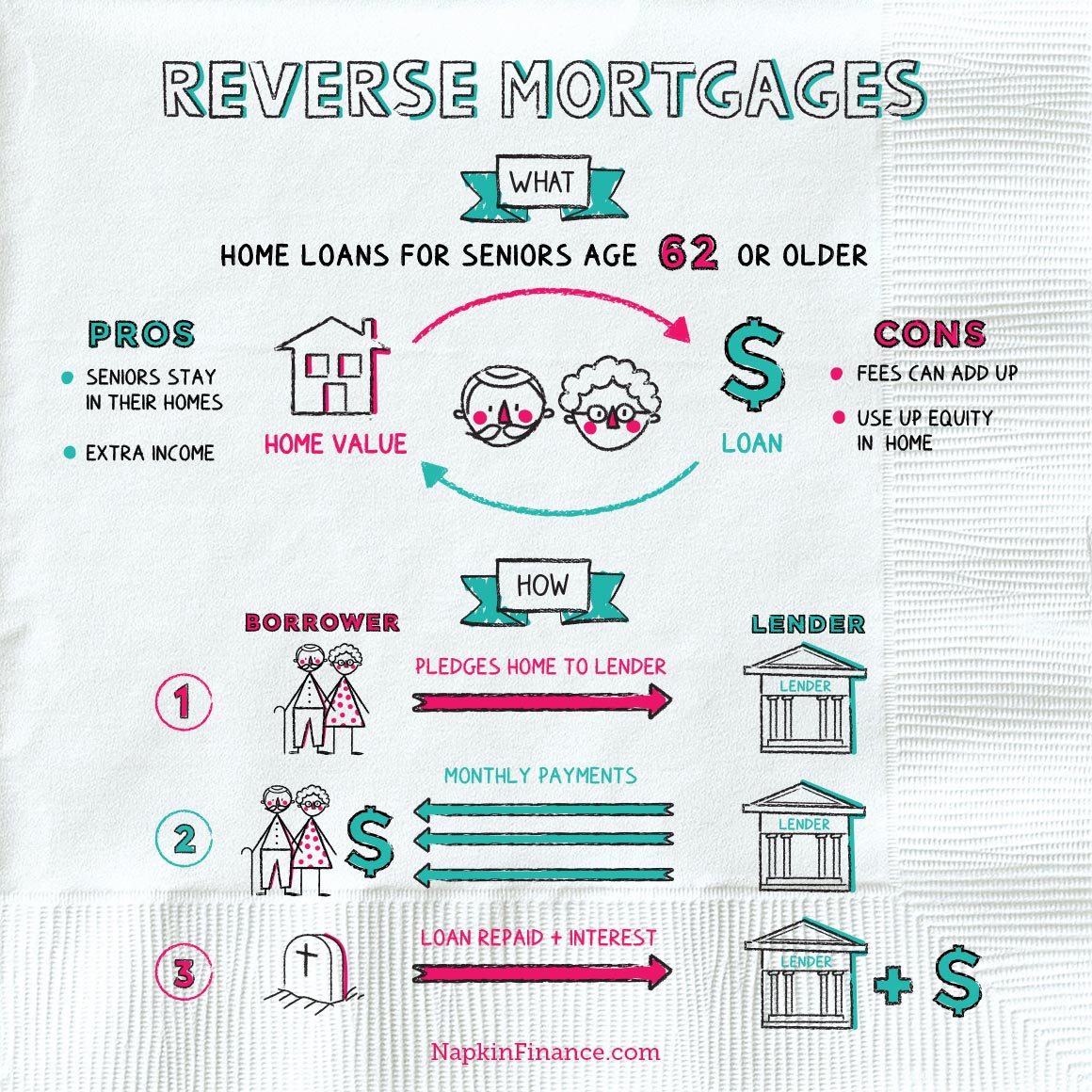

2% in 2004, according to research from the Federal Reserve Bank of St. Louis. As of the second quarter of 2020, it's at 67 (mortgages or corporate bonds which has higher credit risk). 9%. In addition to conventional home mortgages, the FHA offers numerous other loan programs. This is a reverse mortgage program that helps seniors aged 62 and older convert the equity in their houses to money while maintaining title to the home.

This loan consider the expense of particular repair work and renovations into the loan. This one loan permits you to obtain cash for both home purchase and home enhancements, which can make a huge difference if you do not have a lot of money on hand after making a deposit.

The Best Guide To How Does Bank Know You Have Mutiple Fha Mortgages

The concept is that energy-efficient houses have lower operating costs, which lower expenses and make more earnings available for mortgage payments. This is a program for customers who expect their earnings to increase. Under the Area 245(a) program, the Graduated Payment Home loan begins with lower preliminary regular monthly payments that gradually increase over time, and the Growing Equity Home loan has scheduled increases in regular monthly primary payments that lead to shorter loan terms.

If your credit history is between 500 and 579, you may be able to secure an FHA loan if you can pay for a down payment of 10% - what were the regulatory consequences of bundling mortgages. If your credit report is 580 or higher, you can get an FHA loan with a deposit for just 3.

By comparison, you'll usually require a credit report of a minimum of 620, and a down payment between 3% and 20%, to get approved for a traditional home mortgage. For an FHA loanor any kind of mortgageat least two years should have passed considering that the borrower experienced a personal bankruptcy occasion (unless you can demonstrate that the insolvency occasion was because of an unmanageable situation).

If you're delinquent on your federal trainee loans or income taxes, you won't qualify. FHA Loans vs. Traditional Loans 500 620 3. 5% with credit score of 580+ and 10% for credit report of 500 to 579 3% to 20% 15 or 30 years 10, 15, 20, or thirty years In advance MIP + Yearly MIP for either 11 years or the life of the loan, depending on LTV and length of loan None with down payment of at least 20% or after loan is paid for to 78% LTV Upfront: 1.

Unknown Facts About For Mortgages How Long Should I Keep Email

45% to 1. 05% PMI: 0. 5% to 1% of the loan amount per year 100% of deposit can be a present Just part can be a present if deposit is less than 20% Yes No An FHA loan needs that you pay 2 types of mortgage insurance premiums (MIP)an in advance MIP and an annual MIP (which is charged month-to-month).

75% of the base loan amount. You can either pay the in advance MIP at the time of closing or it can be rolled into the loan. For instance, if you're issued a home loan for $350,000, you'll pay an upfront MIP of 1. 75% x $350,000 = $6,125. These payments are transferred into an escrow account that is established by the U.S.

Although the name is somewhat misleading, customers actually make annual MIP payments every month. (To put it simply, yearly MIP payments are not made every year.) The payments vary from 0. 45% to 1. 05% of the base loan quantity. The payment amounts likewise vary depending on the loan quantity, length of the loan, and the original loan-to-value ratio (LTV).

85% of the loan quantity. For instance, if you have a more info $350,000 loan, you will make yearly MIP payments of 0. 85% x $350,000 = $2,975 (or $247. 92 regular monthly). These regular monthly premiums are paid in addition to the one-time upfront MIP payment. You will make annual MIP payments for either 11 years or the life of the loan, depending upon the length of the loan and the LTV.

Examine This Report about How Do Adjustable Rate Mortgages React To Rising Rates

Your lender will evaluate your credentials for an FHA loan as it would any mortgage applicant. Nevertheless, rather of utilizing your credit report, a loan provider may take a look at your work history for the previous 2 years (along with other payment-history records, such as energy and rent payments). As long as you have actually re-established excellent credit, you can still get approved for an FHA loan if you've gone through insolvency or foreclosure.